The fall in activity was mostly limited to small consumer-facing service providers who faced restricted trading conditions and temporary closures.

December data, however, for small manufacturing and construction firms was more positive with survey respondents citing inflows of new work. Many small manufacturers reported a temporary boost to export demand from clients stockpiling ahead of the end of the Brexit transition period as strong growth was seen in both sectors with the rates of output expansion for small firms the quickest since last July and faster than those recorded by larger businesses.

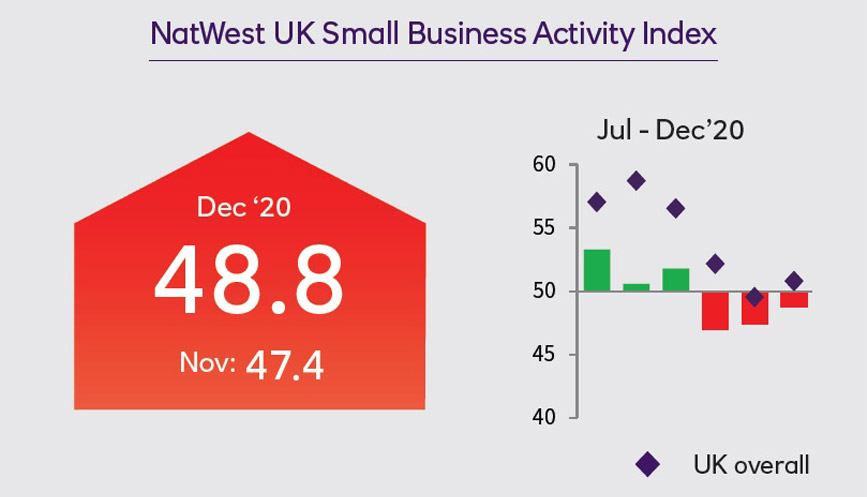

Overall, the headline All-Sector Small Business Activity Index registered 48.8 in December, little-changed from 47.4 in November and in sub-50 contraction territory for a third straight month. The latest reading still lagged behind the equivalent index for UK companies of all sizes, which signalled a slight rise in overall business activity at the end of the year (50.8).

Despite the challenges, small firms retained a positive outlook towards future activity, buoyed by vaccine roll outs and hopes of looser COVID-19 restriction measures over the next 12 months. Optimism improved to the highest since July 2015 but was still weaker than at larger companies.

This positive outlook was not reflected in employment at small firms, which continued to fall. The rate of staff cuts was the quickest since August and faster than at larger firms for the first time since the start of the pandemic.

A rush to bring forward purchases, delays at UK ports, and raw material shortages all contributed to the greatest lengthening of input lead-times since last May. Increased strain on supply chains in turn led to greater upward pressure on input prices in December, with small firms facing the sharpest rise in costs for more than a year and thereby a further squeeze on margins.